Commonwealth of Australia Explanatory Memoranda Commonwealth of Australia Explanatory Memoranda

Commonwealth of Australia Explanatory Memoranda Commonwealth of Australia Explanatory Memoranda[Index] [Search] [Download] [Bill] [Help]

1998-99

THE PARLIAMENT OF THE COMMONWEALTH OF AUSTRALIA

HOUSE OF REPRESENTATIVES

TAXATION LAWS AMENDMENT BILL (No. 4) 1999

EXPLANATORY MEMORANDUM

(Circulated by authority of the

Treasurer, the Hon Peter Costello, MP)

ISBN: 0642 390819

and

Amends the income tax law to allow income tax deductions for gifts made to certain funds and organisations. Amendments are also made to ensure that grants paid to eligible businesses by the Katherine District Business Re-establishment Fund will be exempt from income tax. A number of minor amendments to the gift provisions will also be made.

Date of effect: Various (see Chapters 1 and 2).

Proposal announced: At various times during 1997, 1998 and 1999.

Financial impact: No significant impact on revenue.

Compliance cost impact: Compliance costs will be negligible.

Part 1 amends the Income Tax Assessment Act 1936 to remove the Commissioner of Taxation’s (the Commissioner) power to disregard the ‘notional holder’ rule which public entities may use to calculate the majority underlying interests in their assets. Public entities are listed public companies, publicly traded unit trusts and mutual insurance organisations.

Part 2 amends the Income Tax Assessment Act 1997 to treat all public entities as having had a change in underlying interests at 30 June 1999, unless they can satisfy the Commissioner that they have maintained continuity of majority underlying interests.

Part 3 amends the Income Tax Assessment Act 1997 to ensure that public entities include those that are jointly owned by one or more public entities.

Date of effect: Part 1: 20 January 1997.

Part 2: 30 June 1999.

Part 3: Date of introduction of the Bill into Parliament.

Proposal announced: 1998-99 Budget.

Financial impact: The financial impact for income years, to and including 2000-2001, is estimated to be insignificant. However, it is expected that this measure will increase revenue by $5 million for the 2001-2002 income year and by $10 million for the 2002-2003 income year.

Compliance cost impact: There will be a reduction in compliance costs for public entities that cannot demonstrate continuity of majority ownership as at 30 June 1999. However, there may be an increase in compliance costs for a small number of public entities.

Impact: Low

Main points:

• The taxpayers affected by this measure are public entities. They are listed public companies, publicly traded unit trusts and mutual insurance organisations.

• These taxpayers will need to satisfy the Commissioner that they have maintained continuity of majority underlying interests in their assets.

• It is envisaged that many public entities will immediately realise that they cannot demonstrate continuity of ownership and will reduce their compliance costs by avoiding the time and expense of checking their ownership.

Policy objective: To reduce uncertainty in the practical application of the law and minimise the overall costs of compliance faced by public entities in determining if majority underlying interests have maintained continuity.

Amends the Income Tax Assessment Act 1936 to extend the beneficiary rebate to wages paid to participants in the Community Development Employment Projects (CDEP) Scheme to the extent that they are paid from the wages component of grants made by the Aboriginal and Torres Strait Islander Commission or the Torres Strait Regional Authority.

Impact: Low

Main points:

• The measure will allow participants in CDEP to claim the beneficiary tax rebate so that there is no tax liability on the income support component of their CDEP wages.

• To facilitate claims for the rebate by CDEP participants, the current group certificate requirements will need to be modified.

• The measure will impact on CDEP participants, CDEP employers, third party employers and the Australian Taxation Office.

Amends the Income Tax Assessment Act 1997 (ITAA 1997) by inserting a rewrite of the:

• small business retirement exemption rules that exempt a capital gain; and

• small business roll-over rules that defer a capital gain,

made by an individual, private company or trust (other than a publicly traded unit trust) from a CGT event happening to an asset used in a business.

The amendments will also insert in the ITAA 1997 measures that extend these rules to land and buildings held by a taxpayer where the land and buildings are used by another entity connected with the taxpayer.

Date of effect: The rewrite of the small business retirement exemption and roll-over will apply to assessments for the 1998-99 income year and later income years. The amendments that extend the exemption and roll-over will apply to a CGT event happening to land and buildings after 13 August 1998.

Proposal announced: The rewrite of the small business retirement exemption and roll-over augments the rewrite of the capital gains tax provisions that were inserted in the ITAA 1997 by the Tax Law Improvement Act (No. 1) 1998 (Act No. 46 of 1998). The extension to the exemption and roll-over was announced in the Treasurer’s Press Release No. 76 of 1998 on 13 August 1998.

Financial impact: Only the extension to the exemption and roll-over will have a financial impact. The cost to revenue is difficult to estimate but is not expected to be large.

Compliance cost impact: There are no additional compliance costs associated with either the rewrite of the small business retirement exemption or roll-over. In relation to the measures announced in the Treasurer’s Press Release No. 76 of 1998, it is unlikely that there will be a significant impact on taxpayers’ compliance costs.

Impact: Low

Policy objectives: The Government recognises that many small businesses, for genuine commercial reasons, operate their business through structures that include non-operating entities, which own land and buildings and these assets are used by an entity connected with the non-operating entity.

Amends the ITAA 1997 by inserting a rewrite of the value shifting rules that adjust the cost bases and reduced cost bases of shares and in some cases loans, or underlying interests in them, where there has been a value shift between companies under common ownership. The rules are an anti-avoidance measure that addresses tax deferral.

Date of effect: This amendment will apply to assessments for the 1998-99 income year and later income years.

Proposal announced: The rewrite of the value shifting rules augment the rewrite of the capital gains tax provisions that were inserted in the ITAA 1997 by Act No. 46 of 1998.

Financial impact: None.

Compliance cost impact: There are no additional compliance costs associated with the rewrite.

A Regulation Impact Statement is not required for the rewrite of the value shifting rules.

Amends the ITAA 1997 by inserting a rewrite of the:

• record keeping requirements; and

• rules that disregard a capital gain or loss a taxpayer makes from receiving an amount as reimbursement or payment of expenses under the M4/M5 Cashback Scheme.

The assets register rules allows a taxpayer to transfer some or all of the information contained in records held for capital gains tax purposes into an assets register. The measure will give taxpayers more flexibility in how they keep their records for determining their capital gains tax liability.

The M4/M5 Cashback Scheme is administered by the New South Wales State Government Roads and Traffic Authority. The scheme provides a reimbursement of tolls paid on the M4 and M5 toll roads. The reimbursement is limited to motorists driving motor vehicles and motor cycles privately registered in New South Wales. This amendment will replace the rules that currently exist in Income Tax Regulation 14E.

Date of effect: The amendments will apply to assessments for the 1998-99 income year and later income years.

Proposal announced: These rewritten rules augment the rewrite of the capital gains tax provisions that were inserted in the ITAA 1997 by Tax Law Improvement Act (No. 1) 1998 (Act No. 46 of 1998).

Financial impact: None.

Compliance cost impact: There are no additional compliance costs associated with the rewrites.

A Regulation Impact Statement is not required.

Amends the ITAA 1997 by correcting unintended consequences made by the rewrite of provisions of the Income Tax Assessment Act 1936 (ITAA 1936) that were inserted in the ITAA 1997 by Act No. 46 of 1998. These amendments will make minor drafting and technical changes to these rewritten provisions to more accurately reflect the effect of the ITAA 1936. None of the amendments change the policy reflected in the ITAA 1936.

Date of effect: The amendments will apply to assessments for the 1998-99 income year and later income years.

Proposal announced: The amendments augment the rewritten provisions of the ITAA 1936 that were inserted in the ITAA 1997 by Act No. 46 of 1998.

Financial impact: None.

Compliance cost impact: There are no additional compliance costs associated with the corrections.

A Regulation Impact Statement is not required for the amendments.

Amends the ITAA 1997 by improving the readability of the rewritten provisions of the ITAA 1936 that were inserted in the ITAA 1997 by Act No. 46 of 1998. The amendments correct grammar, insert additional signposts and make slight changes that will improve the wording of the rewrite. There will also be some necessary minor amendments to the ITAA 1936 resulting from Act No. 46 of 1998. None of the amendments change the meaning of the law.

Date of effect: The amendments will apply to assessments for the 1998-99 income year and later income years.

Proposal announced: The amendments augment the rewritten provisions of the ITAA 1936 that were inserted in the ITAA 1997 by Act No. 46 of 1998.

Financial impact: None.

Compliance cost impact: There are no additional compliance costs associated with the amendments.

A Regulation Impact Statement is not required for the amendments.

Amends the Taxation Administration Act 1953 to include the New South Wales Police Integrity Commission (PIC) and the Queensland Crime Commission (QCC) in the definition of ‘law enforcement agency’ and to include the Commissioner for the PIC and the Crime Commissioner for the QCC in the definition of ‘head’ of a law enforcement agency for the purposes of obtaining access to taxation information.

Date of effect: Date of Royal Assent.

Proposal announced: Amendments in relation to the PIC were previously introduced on 2 April 1998 as Schedule 4 to the Taxation Laws Amendment Bill (No. 4) 1998 which lapsed on 31 August 1998. The proposal in relation to the QCC has not been previously announced.

Financial impact: None.

Compliance cost impact: None.

1.1 Schedule 1 to the Bill will amend the Income Tax Assessment Act 1997 (ITAA 1997) to:

• allow income tax deductions for gifts of $2 or more to the funds and organisations listed in paragraph 1.3. This will be done by listing them in the relevant sections of the gift provisions in Division 30 of the ITAA 1997. The index to the gift provisions will also be updated;

• change the name of two organisations listed in Division 30 of the ITAA 1997 to reflect their current names;

• extend the period of time within which donations to the Australian National Korean War Memorial Trust Fund will be tax deductible;

• remove an inconsistency between the terms used in Division 30 of the ITAA 1997 and those used in the Marriage Act 1961 and the Family Law Act 1975; and

• make two minor technical corrections with respect to the National Nurses’ Memorial Trust.

1.2 Schedule 2 to the Bill will:

• amend the ITAA 1997 to allow income tax deductions for gifts of $2 or more to the Katherine District Business Re-establishment Fund; and

• enable grants paid to eligible businesses from that Fund to be treated as exempt income.

1.3 The amendments will result in gifts being tax deductible as follows:

|

Fund/organisation

|

Proposed section and Item reference

|

Special conditions

|

Item number

|

|---|---|---|---|

|

Schedule 1

|

|

|

|

|

Omit ‘The Australian College of Obstetricians and

Gynaecologists’ substitute ‘The Royal Australian and New Zealand

College of Obstetricians and Gynaecologists’

|

Section 30-20(2)

Item 1.2.1 |

None

|

Items 1, 17 and 24

|

|

The Australian Council of Christians and Jews Inc.

|

30-25(2)

Item 2.2.17 |

The gift must be made after 6 December 1998

|

Items 2 and 18

|

|

Sir William Tyree Foundation of The Australia Industry Group

|

30-25(2)

Item 2.2.18 |

The gift must be made after 28 February 1999

|

Items 2 and 25

|

|

The Business Against Domestic Violence Reserve

|

30-45(2)

Item 4.2.15 |

The gift must be made after 22 April 1998

|

Items 3 and 19

|

|

Australian National Korean War Memorial Trust Fund

|

30-50(2)

Item 5.2.6 |

The gift must be made before 2 September 1999

|

Item 4

|

|

Mount Macedon Memorial Cross Restoration, Development and Maintenance Trust

Fund

|

30-50(2)

Item 5.2.8 |

The gift must be made after 8 February 1998

and before 9 February 1999 |

Items 6 and 22

|

|

Omit ‘the Victoria Conservation Trust’ substitute ‘Trust

for Nature (Victoria)’

|

30-55(2)

Item 6.2.6 |

See section 30-60

|

Items 7, 27 and 29

|

|

The Stolen Children’s Support Fund

|

30-70(2)

Item 8.2.2 |

The gift must be made after 28 February 1999

|

Items 9 and 26

|

|

Australian American Education Leadership Foundation Limited

|

30-80(2)

Item 9.2.4 |

The gift must be made after 26 January 1998

|

Items 12 and 16

|

|

Sydney Talmudical College Association Refugees Overseas Aid Fund

|

30-80(2)

Item 9.2.5 |

The gift must be made after 29 January 1998

|

Items 12 and 26

|

|

United Israel Appeal Refugee Relief Fund Limited

|

30-80(2)

Item 9.2.6 |

The gift must be made after 29 January 1998

|

Items 12 and 28

|

|

The Asia Society AustralAsia Centre

|

30-80(2)

Item 9.2.7 |

The gift must be made after 6 December 1998

|

Items 12 and 15

|

|

The Centenary of Federation Trust Fund

|

30-100(2)

Item 12.2.3 |

The gift must be made after 26 November 1998 and before 1 July 2001

|

Items 13 and 19

|

|

St Patrick’s Cathedral Parramatta Rebuilding Fund

|

30-105

Item 13.2.1 |

The gift must be made after 24 February 1998 and before

25 February 2000

|

Items 14 and 26

|

|

Schedule 2, Part 1

|

|

|

|

|

Katherine District Business Re-establishment Fund

|

30-45(2)

Item 4.2.16 |

None

|

Items 1 and 2

|

1.4 Section 30-75 of the ITAA 1997 provides that a gift to a public fund providing money to be used in giving marriage guidance to persons in Australia through a voluntary organisation (or a branch or section of a voluntary organisation) will be deductible only if the organisation (or a branch or section of the organisation) has been declared by the Attorney-General to be a marriage guidance organisation.

1.5 Section 30-75 is being amended to align the taxation law with the criteria used in the Marriage Act 1961 and the Family Law Act 1975 for approval by the Attorney-General of voluntary organisations involved in marriage education, family and child counselling, and family and child mediation. Also, the requirement for the Attorney-General to sign an instrument to certify an organisation has satisfied the criteria is being removed. [Items 8, 10, 11, 20 and 21]

1.6 These amendments will commence on Royal Assent. [Subitem 30(1)]

1.7 The Bill will make minor technical corrections to the ITAA 1997 with respect to the National Nurses’ Memorial Trust. Item 5 renumbers the item reference in subsection 30-50(2) of the ITAA 1997 and Item 23 includes the Trust in the gifts or contributions index in subsection 30-315(2) of the ITAA 1997.

2.1 On 4 June 1998, the Treasurer announced that grants paid as part of a business re-establishment package to eligible businesses and primary producers in those parts of the Katherine region that were devastated by floods in January 1998 will be exempt from income tax.

2.2 The grants (up to a maximum of $10,000 for each business) are paid from the Katherine District Business Re-establishment Fund (the Fund) to provide direct financial assistance to small businesses and primary producers to allow them to recommence business activities and re-establish local jobs.

2.3 Specifically, Part 2 of Schedule 2 will ensure that such a grant paid directly to an eligible taxpayer:

• will be treated as exempt income; [Item 3]

• will not be taken into account in calculating their net exempt income for the purpose of determining whether or not tax losses of earlier income years are deductible; and [Item 4]

• will not give rise to a capital gain. [Item 5]

These amendments only apply in relation to the 1997-98 income year [Item 6] and are in addition to the gift deductible status for gifts or contributions made to the Fund (see paragraph 1.3 in Chapter 1).

3.1 Schedule 3 to the Bill will amend:

• Division 20 of Part IIIA of the Income Tax Assessment Act 1936 (ITAA 1936) to remove the Commissioner of Taxation’s (the Commissioner) power to disregard the ‘notional holder’ rule (see paragraph 3.7) which public entities (listed public companies, publicly traded unit trusts and mutual insurance organisations) may use to calculate the majority underlying interests in their assets.

• Division 149 of the Income Tax Assessment Act 1997 (ITAA 1997) to provide that public entities will be taken to have had a change in majority underlying interests unless the Commissioner is satisfied or is able to reasonably assume that they have maintained the necessary continuity of underlying interests (more than 50%). It will also ensure that public entities include those that are jointly owned by one or more public entities.

3.2 The purpose of the amendments are to:

• provide certainty to public entities which have used the ‘notional holder’ rule to calculate the majority underlying interests in their assets at a test time (within the meaning of Division 20 of Part IIIA of the ITAA 1936) on or after 20 January 1997 to before 30 June 1999;

• treat the assets of public entities as having been acquired after 19 September 1985 unless the Commissioner is satisfied that they have maintained continuity of majority underlying interests in the assets;

• remove the concessional tracing rules including the ‘notional holder’ rule from 30 June 1999; and

• ensure that public entities include those that are jointly owned by one or more public entities.

3.3 The amendments made by:

Part 1 of Schedule 3 applies to a public entity if the test time (within the meaning of Division 20 of Part IIIA of the ITAA 1936) was on or after 20 January 1997;

Part 2 of Schedule 3 applies from 30 June 1999;

Part 3 of Schedule 3 applies from the date of introduction of the Bill into Parliament.

3.4 The Capital Gains Tax (CGT) provisions were originally introduced so that they did not apply to assets acquired by taxpayers before 20 September 1985. This could have allowed post-CGT shareholders to take control of existing companies and benefit from the pre-CGT status of the companies’ assets. Section 160ZZS of the ITAA 1936 provided that an asset acquired by a taxpayer before 20 September 1985 would be deemed to have been acquired on or after that date unless the Commissioner was satisfied or considered it reasonable to assume that continuity of majority underlying interests in the asset had been maintained.

3.5 Amendments were made to the ITAA 1936 in 1997 to make the rules expressed in section 160ZZS apply more appropriately to public entities. Division 149 of the ITAA 1997 reflect the provisions of Division 20 of Part IIIA of the ITAA 1936, including those amendments.

3.6 Under the arrangements in Division 149 of the ITAA 1997, public entities which had not previously been required to test, or had maintained continuity of underlying interests must determine whether the majority underlying interests in the assets owned by the public entity have changed since 19 September 1985. Public entities which had a change in majority underlying interests are taken to have acquired the asset for its market value on the date of the test, not the date when continuity was lost.

3.7 The current rules provide a range of streamlined tracing measures intended to help public entities in carrying out the test. All shareholdings or unitholdings in a public company or publicly traded unit trust that are less than 1% are taken to be owned in aggregate by a single notional holder (‘notional holder’ rule). Public entities, when testing for continuity of majority underlying interests may assume that the interests held by the notional holder have not changed. In practical terms, public entities with large notional holder interests (more than 50%), do not need to look further to demonstrate they have maintained continuity of majority underlying interests. However, this ‘notional holder’ rule is disregarded by the Commissioner if it gives an inappropriate result. That is if it produces continuity of majority underlying ownership that would not otherwise exist. Direct and indirect holdings of complying superannuation funds, complying approved deposit funds, foreign superannuation funds, certain companies and government bodies may in certain circumstances be treated as held by natural persons who held all the interests of the relevant fund, company or government body.

3.8 Effectively, for certain classes of shareholder or unitholder, a public company or publicly traded unit trust may choose not to identify the actual individuals who hold underlying interests in its assets. There is also a special concession provided where a mutual insurance organisation demutualises. Broadly, on demutualisation the members who are issued shares on demutualisation will be taken to have held those interests in the demutualised entities assets since 19 September 1985.

3.9 In the Government’s 1998-99 Budget Statement, the Treasurer announced that measures would be introduced to ensure that all public entities will be taken to have had a change in majority underlying interests at 30 June 1999, unless they satisfy the Commissioner that they have maintained continuity of majority underlying interests. Further, that the concessional tracing rules including the ‘notional holder’ rule would be removed.

3.10 Public entities which, despite relying on the ‘notional holder’ rule, cannot demonstrate continued majority underlying interests on the first test time of 20 January 1997 will still be required to examine their records to find the earliest time they were required under a public ruling issued by the Commissioner to examine their records for changes in majority underlying interests. Such assets will be treated as being acquired at market value on that earlier date.

3.11 Public entities that cannot demonstrate continued majority underlying interests for test times after 20 January 1997 will be taken to have acquired those assets at market value at that test time.

3.12 Removal of the Commissioner’s power to disregard the ‘notional holder’ rule enables a public entity, which has used that rule to determine the majority underlying interests in its assets at a test time (within the meaning of Division 20 of Part IIIA of the ITAA 1936) on or after 20 January 1997 and before 30 June 1999, to rely on that determination.

3.13 However, from 30 June 1999, other amendments in the Bill remove the ability for public entities to use the ‘notional holder’ rule – refer to the ‘tracing rules’ section for further explanation (see paragraphs 3.19 to 3.23).

3.14 If public entities with a pre-CGT asset wish to retain their pre-CGT status, they must, within 6 months after the test day, give the Commissioner written evidence about the majority underlying interests in the asset on the test day. A test day is any of the following:

• 30 June 1999;

• every 5 years from that date; and

• a day where abnormal trading of shares in the company or units in the publicly traded unit trust, as the case may be, occurs. Abnormal trading is defined in Subdivision 960-H of the ITAA 1997 which sets out the relevant factors that must be taken into account. [New subsections 149-55(1) and (2)]

3.15 The evidence is to be given to the Commissioner in a form that makes the information about the asset’s majority underlying interests readily apparent. [New subsection 149-55(1A)]

3.16 The only consequence of a public entity, with a pre-CGT asset, not giving the Commissioner written evidence about the asset’s majority underlying interests is that the asset will stop being a pre-CGT asset from the test day the entity fails to provide the evidence. It is not a taxation offence if the entity fails to give the evidence. [New subsection 149-55(1B)]

3.17 The Commissioner must be satisfied, or think it reasonable to assume, from the evidence that continuity of majority underlying interests in the asset has been maintained from the starting day to the test day. The starting day is either:

• 19 September 1985; or

• a day chosen by the entity during the period from 1 July 1985 to 30 June 1986 which could be demonstrated is a reasonable approximation of the owners who had underlying interests in the entity’s assets on 19 September 1985. [New section 149-60]

3.18 If the evidence:

• is not given to the Commissioner within 6 months after the test day; or

• fails to satisfy the Commissioner that continuity of majority underlying interests in the asset has been maintained the asset stops being a pre-CGT asset. [New section 149-70]

3.19 The current tracing rules contained in Subdivisions 149-D and 149-E of the ITAA 1997 are considered to be unsatisfactory.

3.20 On one hand public entities may, for the purposes of the test, assume that registered holdings of less than 1% have always been held by a single ‘notional holder’ rule. On the other hand the Commissioner has the discretion to disregard the ‘notional holder’ rule if the Commissioner is satisfied that there has in fact been a change in majority underlying interests in the asset.

3.21 These amendments, therefore, repeal Subdivisions 149-D and 149-E and remove the current law’s uncertainty.

3.22 Public entities with pre-CGT assets will, however, from 30 June 1999 be required to test using less concessional rules. It will be assumed they have failed unless they provide written evidence to the Commissioner, within 6 months after the test day, which satisfies the Commissioner that there has not been a change in majority underlying interests in the asset.

3.23 In view of the period that has elapsed since the commencement of the CGT regime (19 September 1985) it is expected that only a handful of public entities will be able to provide evidence to satisfy the Commissioner that there has not been a change in majority underlying interests in their pre-CGT assets. If a public entity’s assets are to be treated as post-CGT assets, the asset’s cost base is its market value at the test day it stops being a pre-CGT asset – initially 30 June 1999.

3.24 The Part 3 amendment items clarify the intention of the current law in relation to interposed entities. One interpretation of the current Subdivision 149-C of the ITAA 1997 is that it does not treat all wholly-owned subsidiaries of public entities as public entities.

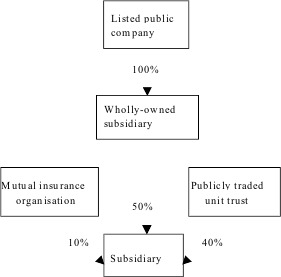

3.25 To remove any doubt, the amendments make it clear that Subdivision 149-C applies to all wholly-owned, directly or indirectly, subsidiaries of public entities, including those that are jointly owned by one or more public entities. [New paragraphs 149-50(1)(e) and 149-55(2)(d)]

A subsidiary that is 100% owned, directly or indirectly, by a mutual insurance organisation (10%), a listed public company via a wholly-owned subsidiary (50%) and a publicly traded unit trust (40%) will be treated as a public entity.

3.26 On 18 December 1998 the Commissioner announced that under Division 20 of Part IIIA of the ITAA 1936 and Division 149 of the ITAA 1997 public entities would not have to complete their determinations for the test time of 20 January 1997 and any subsequent test time until one month following the date of Royal Assent of this Bill. Public entities should ensure that they make the necessary determinations within this time.

3.27 Public entities can rely on the ‘notional holder’ rule to make any determinations for any test time up until 30 June 1999. It is possible that some public entities have already made determinations without relying on the ‘notional holder’ rule. These entities may make a new determination properly relying on the ‘notional holder’ rule before the extended time to make determinations ends.

3.28 The Government would like to reduce uncertainty in the practical application of the law and minimise the overall costs of compliance currently faced by public entities in determining if majority underlying interests have maintained continuity of ownership of their assets.

3.29 A measure to address this objective was announced by the Treasurer in his 1998-99 Budget.

3.30 The CGT provisions were designed not to apply to pre-CGT assets. Companies and similar entities present a difficulty for this rule, because of the possibility of retaining pre-CGT status for assets of a company that has been sold post-CGT. Therefore, section 160ZZS of the ITAA 1936 provided that assets acquired by a company or similar entity before 20 September 1985 would be treated as acquired on or after that date unless the Commissioner was satisfied or considered it reasonable to assume that there had been continuity of majority underlying interests in the assets. Section 160ZZS of the ITAA 1936 has been rewritten as sections 149-30 and 149-35 of the ITAA 1997.

3.31 Public entities faced considerable difficulties determining whether the majority underlying interests in the assets of the public entity had maintained continuity. This was particularly the case where a public entity had a large number of shareholders or unitholders where shares or units are constantly being traded.

3.32 As part of the 1996-97 Budget on 20 August 1996, the Government announced amendments to the rule expressed in section 160ZZS. The amendments allowed public entities which had so far not had to test or had maintained continuity of majority underlying interests to periodically test on prescribed dates (commencing on 20 January 1997, every 5 years thereafter, and whenever there is abnormal trading) to determine whether they had maintained continuity of majority underlying interests in their pre-CGT assets. If it is found continuity is not maintained at the test time, the pre-CGT assets of the entity will be taken to be acquired at the test time for their market value. This test has the benefit of a generous ‘notional holder’ rule (which broadly allows listed public companies and publicly traded unit trusts to treat registered holders of less than 1% as being owned by a single notional holder) which the Commissioner is to override if it appears likely to produce a wrong result in substance.

3.33 However, this power given to the Commissioner, as a result of the 1996-97 Budget changes, has caused public entities to be uncertain of their ability to rely on their determination when they have used the ‘notional holder’ rule. Public entities have also experienced increased compliance costs as a result of these changes.

3.34 The measure proposes that public entities’ pre-CGT assets held at 30 June 1999 be treated as post-CGT assets unless they can provide the Commissioner with sufficient evidence to be satisfied or reasonably assume that they have maintained continuity of majority underlying interests in their pre-CGT assets.

3.35 Under the measure, in the period to 30 June 1999, the test of whether an entity has maintained continuity of majority underlying interests in its pre-CGT assets will be determined by the application of the currently enacted law. The benefit of the ‘notional holder’ rule is retained but not the discretion available to the Commissioner to override that rule where it would produce a wrong result in substance (Part IVA of the ITAA 1936 – the general anti-avoidance provisions – would still be relied on in the case of artificial avoidance).

3.36 These amendments are the only option for implementing the Government’s policy objective.

3.37 The affected groups are ‘public entities’ within the meaning of Division 149 of the ITAA 1997 (rewritten Division 20 of Part IIIA of the ITAA 1936) who hold pre-CGT assets. The measure will make it very clear that Division 149 applies to all ‘100% subsidiaries’ of public entities, including those that are wholly-owned by one or more public entities. For example, a subsidiary that is 100% owned, directly or indirectly, by a mutual insurance organisation (10%), a listed public company via a wholly-owned subsidiary (50%) and a publicly traded unit trust (40%).

3.38 It is expected that the measure will reduce the Australian Taxation Office’s (ATO) administration costs.

3.39 Quantitative data on the compliance and administrative costs of the measure is not available. Consequently, the assessment is of a qualitative nature.

3.40 Having public entities’ pre-CGT assets treated as post-CGT assets from a prescribed date unless they could demonstrate continuity of ownership of those assets, would reduce compliance costs to a considerable degree. This is because public entities would not have to test their continuity of ownership every five years and whenever there is abnormal trading. All affected public entities will need to get a market valuation for their pre-CGT assets on 30 June 1999. Thereafter, compliance costs will be small.

3.41 The measure will reduce compliance costs as most public entities will not demonstrate continuity of majority ownership as at 30 June 1999.

3.42 A public entity will be taken to have had a change in majority underlying interests unless it can demonstrate continuity of ownership at 30 June 1999, and thereafter every 5 years or at a time of abnormal trading. To avoid being taken to have had a change in majority underlying interests, the Commissioner must be satisfied, or think it reasonable to assume, from the evidence provided by the public entity that there has not been a change in majority underlying interest in its assets. This may be a costly exercise for public entities with widespread ownership.

3.43 It is envisaged that many public entities will immediately realise that they cannot demonstrate continuity of ownership and avoid the time and expense of checking their ownership. Public entities which believe they have had a change in majority underlying interests will not have to make a determination to that effect (as is currently required). This may also provide some public entities with cost savings.

3.44 However, a small number of public entities may be able to demonstrate to the Commissioner that they have maintained continuity of ownership. For these entities there is no reduction in compliance costs. These public entities, may face a higher cost of compliance than under the current arrangements, as they will be required to satisfy the Commissioner that they have maintained continuity of majority underlying interests in their assets, without the benefit of the current concessional tracing rules.

3.45 ATO administration costs are also expected to be reduced by this measure.

3.46 It is expected that the revenue impact of the measure will be as follows:

1997-1998 insignificant*

1997-1999 insignificant*

1999-2000 insignificant *

2000-2001 insignificant

2001-2002 +$5 million

2002-2003 +$10 million

*Note: The estimated revenue forecasts for the amendments to Division 20 of Part IIIA of the ITAA 1936 announced in the 1996-97 Budget Statement have been revised down to ‘insignificant’ for the years 1997 to 2000 as a result of new data becoming available, which shows that collections under that amendment would be substantially deferred from those originally projected.

3.47 The measure was developed in consultation with taxpayer representative bodies (Corporate Tax Association, Institute of Chartered Accountants, Australian Society of Certified Practicing Accountants, Taxation Institute of Australia, National Institute of Accountants, Business Council of Australia and the Law Council of Australia).

3.48 The proposed measure will not disadvantage public entities that can demonstrate continuity of majority underlying interests. These public entities will retain the pre-CGT status of their assets.

3.49 The proposed measure will improve certainty during the period to 30 June 1999 by allowing public entities to rely on the ‘notional holder’ rule to assume continuity without risk of being overridden. If a public entity does not pass the continuity test at 30 June 1999, the cost base of each asset will be calculated at that date. Also, public entities that cannot demonstrate continuity of majority ownership will have reduced compliance costs.

4.1 Schedule 5 to the Bill will amend the Income Tax Assessment Act 1936 (ITAA 1936) to enable participants in the Commonwealth Development Employment Projects (CDEP) Scheme to claim the beneficiary tax rebate in respect of the income support component of their CDEP wages.

4.2 To extend the beneficiary rebate to the income support component of wages paid to CDEP participants sourced from CDEP wage grants provided by the Aboriginal and Torres Strait Islander Commission (ATSIC) and the Torres Strait Regional Authority (TSRA).

4.3 The amendments will commence on the date of Royal Assent and will apply to payments made on or after 1 July 1998. [Item 2]

4.4 The CDEP Scheme is administered by ATSIC and TSRA to enable Indigenous Australian communities and organisations to manage their own economic and social development and to provide employment for people in their communities.

4.5 To participate in the scheme, unemployed members of the Indigenous communities choose to give up their entitlements to social security payments, for example, the Newstart Allowance. In place of the social security payments forgone, the community organisations pay wages to participants to undertake community managed activities out of the income support component of grants provided by ATSIC and the TSRA.

4.6 Section 160AAA of the ITAA 1936 provides a rebate, called the beneficiary rebate, to recipients of certain Commonwealth benefits. For example, recipients of the Newstart Allowance (who may work for their unemployment benefits) and participants in labour market programs such as Green Corps and the New Enterprise Incentives Scheme are entitled to the beneficiary rebate on the assessable income they receive from these programs.

4.7 The income support component of CDEP wages technically falls outside the scope of payments that are rebatable under section 160AAA of the ITAA 1936 because of the nature and calculation of the funding of the CDEP scheme.

4.8 The proposed amendment is in response to a recommendation by the Independent Review of the Community Development Employment Projects Scheme known as the Spicer Review. The extension of the beneficiary rebate to CDEP participants will remove the taxation disincentive for joining and remaining a participant in the CDEP scheme.

4.9 The proposed amendment will provide that the income support component of CDEP wages will be rebatable under section 160AAA of the ITAA 1936. In particular, Item 1 of Schedule 5 inserts new paragraph 160AAA(1)(c), which will allow CDEP participants to claim the beneficiary tax rebate in respect of the income support component of their CDEP wages. Other components of the CDEP wage will not be rebatable.

Fred is a married participant in the CDEP Scheme and receives wages from his CDEP employer of $24,500. $21,000 is paid by way of income support from the ATSIC wages grant. Fred’s tax liability will be calculated as follows:

Tax on $24,500 4,352.00

Plus Medicare levy calculated on $24,500 367.50

Less rebate of ($21,000 – $5,400) x 20% 3,120.00

Less rebate of ($21,000 - $20,700) x 14% 42.00

Total liability $1,557.50

4.10 The proposed amendments will apply to payments made on or after 1 July 1998. [Item 2]

4.11 It is also proposed to amend the Income Tax Regulations to require CDEP employers to identify the income support component of CDEP wages separately on group certificates. The amendment is required to ensure that participants know how much of their CDEP wage is rebatable when completing their personal income tax return.

4.12 The policy objective of this measure is to remove a taxation disadvantage suffered by participants in the CDEP Scheme, compared with Newstart recipients and participants in other Commonwealth labour market programs, by allowing them to claim the beneficiary tax rebate in respect of the income support component of the CDEP wages.

4.13 The Government announced this measure in the 1998-99 Budget so that it will apply to claims for the beneficiary rebate in respect of wages paid to CDEP participants from 1 July 1998.

4.14 Wages paid to CDEP participants may consist of amounts paid from sources other than the wages component of grants from ATSIC and TSRA. For example, CDEP wages may consist of ‘top-up’ amounts from profits made by the community organisations or from other Government sources. Payments may also be received from the operational funds grant from ATSIC and TSRA.

4.15 Under the current tax law CDEP employers are required to provide CDEP participants with a group certificate detailing the gross amount of salary or wages. Whilst ATSIC and TSRA require community organisations to account for the wages grant separately, CDEP employers are under no obligation to advise CDEP participants of the income support component of their CDEP wages.

4.16 The only implementation option considered feasible was to amend section 160AAA of the ITAA 1936 to provide that the income support component of CDEP wages will be rebatable.

4.17 The implementation option required consideration of how to impose an obligation on CDEP employers to advise CDEP participants of the income support component of their CDEP wages. Participants in the CDEP Scheme need to know what part of their CDEP wage is rebatable so they can claim their rebate entitlement in their tax return.

4.18 The obligation could be imposed on employers by amending the ITAA 1936. Given the number of employers affected, this option is considered impracticable. The preferred approach is to amend the Income Tax Regulations to require CDEP employers to specify the income support component amount of CDEP wages separately on group certificates.

4.19 One of the key outcomes of extending the beneficiary rebate to the income support component of CDEP wages is to eliminate the need for CDEP participants with no other sources of income to lodge tax returns. To achieve this outcome the Commissioner of Taxation has facilitated the lodgement of blanket tax instalment variations by CDEP employers under section 221D of the ITAA 1936.

4.20 Generally speaking, once a variation is approved, the CDEP employer is no longer required to deduct tax instalment deductions from the income support component of the CDEP participant’s wage. If the CDEP participant has no other source of income, no tax return is required.

4.21 While it is proposed to impose an obligation on employers who pay CDEP wages, it is not intended to change group certificate stationery or specifications for electronic group certificates to provide for the separate disclosure of the income support component of CDEP wages on the group certificates. Changing existing stationery could increase compliance and administrative costs on all group employers, as those not affected by the measure may nonetheless inquire about the change.

4.22 Rather, employers who pay rebatable CDEP wages will need to adapt existing group certificate stationery and payroll systems in order to show the income support component of those wages.

4.23 The proposal will affect the following groups:

• CDEP participants;

• CDEP employers and third party employers;

• Australian Taxation Office (ATO).

4.24 CDEP participants may incur additional costs in learning about the tax change and ensuring tax instalment deductions are varied where their employer has not applied for a blanket variation.

4.25 The net compliance cost impact on CDEP participants should be minimal and limited to the year in which the measure is introduced.

4.26 Approximately 240 CDEP community organisation employers will be affected. An unknown number of third party employers contracted by community organisations to provide training to participants will also be affected.

4.27 Payers of CDEP wages will need to learn about the change, seek 221D variations, vary tax instalment deductions and separately notify CDEP participants of the amount of the income support component of CDEP wages paid. Additional costs will be incurred in adapting current group certificate stationery and payroll systems in order to show the income support component of CDEP separately.

4.28 The changes are expected to impose initial compliance costs of less than $200,000. Most of these will be incurred by those CDEP employers who need to change PAYE systems. Recurrent costs from the changes are expected to be minimal.

4.29 There are approximately 32,000 CDEP participants who will be affected by the proposed amendment. Approximately two thirds of CDEP participants live in remote areas and will no longer be required to lodge returns as the beneficiary rebate along with low income and zone rebates should extinguish any tax liability. A large number of the remaining one third not in remote areas receive additional wages that will not be rebatable, so will still be required to lodge tax returns. Where returns are no longer required, compliance costs will be reduced.

4.30 The ATO will need to devote additional resources in providing information support to the impact support groups. The ATO will provide information to individuals, community organisations and third party employers through field visits, direct mailing of information, and via TaxPack.

4.31 CDEP community organisations have all been sent information concerning the application of section 221D variations, which they need to fill out so the Commissioner can allow them to reduce the tax instalments from the income support component of CDEP wages paid to participants to nil.

4.32 They have also been provided with a briefing and examples to assist them to implement these changes and advise participants. The ATO has officers visiting Indigenous communities and CDEP community organisations advising of the changes. ATSIC has also provided briefings through their networks.

4.33 The ATO anticipates some small administrative savings from the small reduction in the number of tax returns lodged. These savings will be partly offset by monitoring applications for blanket section 221D variations and improved compliance strategies to ensure that taxpayers receive the correct benefit.

4.34 Based on the number of participants likely to experience tax liabilities in respect of the income support component of their CDEP wages, the measure will cost the revenue approximately $7 million in 1998-99 and $7 million in each subsequent income year.

4.35 The group certificate changes will only apply to payments made on or after 1 July 1999. Community organisations will be required under the ATSIC and TSRA terms and conditions of grants to advise third party employers of the income support component of the payments they make on or after 1 July 1999.

4.36 For the 1998–99 year of income, the ATO, ATSIC and TSRA will ask community organisations to request third party employers to advise CDEP participants the amount of any income support component paid to them. However, there is no obligation on them to do so in the 1998-99 year of income.

4.37 In order to develop the best policy for implementation, numerous people from various different organisations were consulted. ATO Aboriginal liaison officers visited Aboriginal CDEP community organisations and participants to gauge their opinions. ATSIC was also involved throughout the project.

4.38 Accountants, employers, computer systems experts and payroll software providers were involved in providing advice about ways in which to minimise compliance costs.

4.39 Implementation of this tax measure removes a current inequity in the income tax law by ensuring that CDEP participants receive equivalent tax treatment to other social welfare recipients.

4.40 Whilst this tax measure has the effect of increasing compliance costs for CDEP employers, the supporting modifications to the current group certificate arrangements will provide employers with some flexibility in terms of the provision of information to participants.

4.41 The ATO and Treasury will monitor this measure, as part of the whole taxation system, on an continuing basis.

5.1 The amendment contained in Schedule 5 Part 1 Item 1 to the Bill will amend the Income Tax Assessment Act 1997 (ITAA 1997) by inserting a rewrite of the small business retirement exemption rules that exempt a capital gain made by an individual, private company or a trust (other than a publicly traded unit trust) from a CGT event happening to an asset used in a business.

5.2 The amendment will also insert in the ITAA 1997, measures that extends this exemption to land and buildings held by a taxpayer where the land and buildings are used by another entity connected with the taxpayer.

Part A provides an explanation of the rules about small business retirement exemption.

Part B lists provisions that have not been rewritten.

Part C provides a Regulation Impact Statement for the amendments that relate to land and buildings.

5.3 Division 17B of Part IIIA of the Income Tax Assessment Act 1936 (ITAA 1936) provides an exemption from tax for capital gains made on a CGT event happening to the assets of a small business where the proceeds are used for retirement.

5.4 Division 17B was inserted in the ITAA 1936 by Taxation Laws Amendment Act (No. 3) 1997 (Act No. 147 of 1997). Amendments to this Division were made by Taxation Laws Amendment Act (No. 1) 1998 (Act No. 16 of 1998).

5.5 The measure will extend these provisions to assets held by a taxpayer that is not carrying on a business if the assets are used by another entity connected with the taxpayer in the course of carrying on a business.

5.6 Division 17B is translated as Subdivision 118-F. No changes have been made to the substance of Division 17B in the course of its translation into the rewrite other than the above.

5.7 The Joint Committee of Public Accounts and Audit (JCPAA) reviewed the rewritten ITAA 1936 provision contained in the Tax Law Improvement Act (No. 1) 1998 (Act No. 46 of 1998). The JCPAA tabled their findings in Parliament on 12 March 1998 as Report 356: An Advisory Report on the Tax Law Improvement Bill (No. 2) 1997. Recommendation 3 of that report requested (among other things) delaying the introduction of the rewritten small business retirement exemption provisions pending further review by the JCPAA.

5.8 The JCPAA findings in that further review was tabled in Parliament on 21 December 1998 as Report 364: An Advisory Report on the Delayed Provisions of the Tax Law Improvement Bill (No. 2) 1997.

5.9 The amendments discussed in this Chapter reflect recommendation 3 of Report 356 and recommendation 3 of Report 364 made by the JCPAA.

5.10 The rewrite of the small business retirement exemption will apply to assessments for the 1998-99 income year and later income years [Part 5 Item 35]. The date of effect reflects the view expressed by the JCPAA in Report 364 paragraphs 2.9 to 2.12. The extension to the exemption will apply to a CGT event happening to land and buildings after 13 August 1998. [Item 2, new section 123-80]

5.11 In qualifying situations the Subdivision exempts a capital gain made by an individual, private company or trust (other than a publicly traded unit trust) from a CGT event happening to an asset used in a business or an intangible asset (such as goodwill) inherently connected to the business. For example, a sale of such an asset would be a CGT event.

5.12 The Treasurer announced in Press Release No. 76 of 1998 that the small business retirement exemption would be extended to include land and buildings held by a taxpayer if the land and buildings are used by another entity connected with the taxpayer. The extension to the exemption is achieved by modifying the definition of ‘active asset’. The extension will apply to a CGT event happening to land and buildings after 13 August 1998. [Item 2, new section 123-80]

5.13 A taxpayer can disregard a capital gain if the requirements for exemption are satisfied. Generally these are:

• the asset must be an active asset;

• the net value of the taxpayer’s CGT assets (and that of other entities related to the taxpayer) must not exceed $5,000,000;

• the capital proceeds from the sale must be received within the period one year before, and ending 2 years after, the time of the CGT event happening; and

• if the capital proceeds give rise to an eligible termination payment (ETP) and the recipient is under 55 years of age, the ETP must be rolled-over.

5.14 For a company or trust, the exemption is also available if there is a controlling individual of the company or trust and the capital proceeds are paid to the controlling individual as an ETP. [New section 118-405]

5.15 There are separate tests for determining whether an individual is a controlling individual of:

• a company;

• a trust with fixed entitlements to income and capital; or

• a trust where the income and capital entitlements are not fixed.

The tests generally require that the individual be entitled to at least 50% of all distributions of the company or trust. [New section 118-410]

5.16 There are other consequences if a taxpayer choose to treat part of a capital gain as exempt. There can be no roll-over for the CGT event and exemptions for goodwill and main residence cannot apply to any balance of the capital gain.

5.17 The capital proceeds that the taxpayer receives as a controlling individual are treated as an ETP. [New section 118-415]

5.18 The capital gain that the taxpayer can choose to treat as exempt is a CGT exempt amount. The CGT exempt amount is calculated as follows:

Step 1: Reduce the capital gain by any net capital loss the taxpayer may have, and would have applied in calculating a net capital gain in respect of the asset.

Step 2: Ensure that the remaining capital gain does not exceed the relevant CGT retirement exemption limit.

Step 3: If the asset was owned by a company or trust that was not controlled by the same individual for one of the following periods:

• start of the 1992-93 income year to just before the time of the CGT event; or

• when the asset was acquired to just before the time of the CGT event;

the Step 2 amount is further reduced. [New sections 118-420, 118-425 and 118-430]

5.19 An individual’s CGT retirement exemption limit is $500,000 reduced by any previous exemptions the individual has received under these rules. [New section 118-435]

5.20 There are detailed rules:

• for determining the maximum net value of the taxpayer’s assets and those of entities related to the taxpayer; [New section 118-440]

• for determining when an asset needs to have been an active asset; [New section 118-445] and

• that deal with the making of an ETP by a company or trust. [New section 118-450]

5.21 The following provisions are redundant and have not been rewritten.

|

Provision

|

Subject

|

Reason for omission

|

|---|---|---|

|

160ZZPZAA

|

Application provision continuing operation of Division 17B to assessment

for income years beyond 1997-98

|

Operation of Division 17B closed off due to inserting the rewritten

Division in the ITAA 1997.

|

|

160ZZPZB(1)

|

Sign posts reader to which Subdivision applies to individuals

|

Redundant

|

|

160ZZPZB(2)

|

Sign posts reader to which Subdivision applies to companies and

trusts

|

Redundant

|

|

160ZZPZB(5)

|

Sign posts reader to Subdivision containing definitions

|

Redundant

|

|

160ZZPZH(1)

|

Guide material

|

Redundant

|

|

160ZZPZI(1)

|

Guide material

|

Redundant

|

|

160ZZPZI(3)

|

States second condition before being able to apply the exemption

|

Subsumed by the structure of the rewrite

|

|

160ZZPZJ(1)

|

Guide material

|

Redundant

|

|

160ZZPZL(6)

|

Provides an example

|

Redundant

|

|

160ZZPZM

|

Lists expressions used in the Division

|

The Dictionary in the ITAA 1997 removes the need for this provision

|

|

160ZZPZP(1)

|

Guide material

|

Redundant

|

5.22 The Government announced in the Treasurer’s Press Release No. 76 of 1998, its intention to extend the capital gains tax (CGT) small business roll-over and retirement exemption initiatives.

5.23 The extended measures will allow a taxpayer to defer a capital gain under the roll-over provisions or seek an exemption from CGT in certain circumstances where a CGT event happens to land and buildings. Typically, this would apply to cases where land and buildings are owned by an entity that does not operate a business (non-operating entity) though these assets are used by another entity in carrying on a business (operating entity) and the two entities are either:

• connected (interlocking control); or

• an individual controls both entities (common control).

5.24 The Government recognises that many small businesses, for genuine commercial reasons, operate their businesses through structures that include non-operating entities, which own land and buildings and these assets are used by a connected entity.

5.25 The new measures are to operate for all CGT events happening to land and buildings after 13 August 1998. All of the existing conditions for the CGT roll-over and retirement exemption will continue to apply.

5.26 The small business roll-over allows taxpayers to defer tax on capital gains made on a CGT event happening to a business asset, shares in a company or units in a unit trust, if the taxpayer acquires a replacement business asset or other shares or units.

5.27 The small business retirement exemption allows a taxpayer to claim an exemption from CGT on a CGT event happening to a business asset used to fund the retirement of an individual.

5.28 The new measures are designed to extend the existing small business roll-over and the retirement exemption provisions, to provide CGT roll-over or retirement exemption where small business structures have non-operating entities that own land and buildings that are used by an operating entity.

5.29 In considering the Government’s intention to extend the current small business roll-over and retirement exemption only one option was considered: amending the CGT provisions of the ITAA 1997 to give effect to the following features:

• to extend the CGT small business roll-over and retirement exemption to include a CGT event happening to land and buildings owned by a non-operating entity;

• to classify land and buildings as being an ‘active asset’ of the business if it is used, or is held ready for use by the taxpayer, in carrying on the business or by an entity that is the taxpayer’s ‘connected entity’ or ‘small business CGT affiliate’;

• if the non-operating entity’s replacement asset in obtaining small business roll-over is a share in a company or unit in a unit trust, the taxpayer or an entity connected with the taxpayer must be a controlling individual of the company or trust just after the taxpayer acquires the shares or units; and

• if the replacement assets are shares in a company or units in a unit trust, a capital gain will accrue to the taxpayer if the taxpayer, or another entity connected with the taxpayer, ceases to be a controlling individual of that company or trust. This would also apply where that other entity, which is a controlling individual, ceases to be connected with the taxpayer.

5.30 The implementation option reflects the Government’s original policy intention, and removes a potential anomaly which could have been introduced if the Treasurer’s Press Release No. 76 was strictly adhered to.

5.31 The new measures will impact on small business taxpayers providing they meet the existing small business roll-over or retirement exemption rules. This includes:

• small business taxpayers that roll-over land and buildings, integral to the operating entity, into either other business assets (including land and buildings), shares in a company or units in a unit trust; and

• small business taxpayers who dispose of land and buildings, in addition to other business assets to fund the retirement of the taxpayer.

5.32 Professional advisers to small business will also be affected by the measure.

5.33 The Australian Taxation Office (ATO) will administer these measures.

5.34 The proposal will impose additional requirements on taxpayers and professional advisers. Small business taxpayers and their advisers will need to become familiar with the new measures. Some taxpayers will need to keep additional records, and to provide copies of those records to the ATO to satisfy the small business roll-over threshold. Others will have to provide copies of existing records to the ATO in order to demonstrate compliance with the threshold. These requirements are unlikely to have a significant impact on taxpayers’ compliance costs and have not been quantified.

5.35 The ATO does not expect the measures to require more resources beyond those already allocated to the current small business roll-over and the retirement exemption.

5.36 The cost to revenue for the proposal is difficult to estimate (primarily due to a lack of reliable data), but it is not expected to be large. This cost will be monitored by the ATO.

5.37 the ATO and Treasury were consulted about the proposed measures. Previously, small businesses and Treasury were consulted.

5.38 The Government proposes to extend existing CGT small business roll-over and retirement exemption to all small businesses who, for genuine commercial reasons, operate their business through structures that include non-operating entities which own land and buildings, if these assets are used by a connected operating entity.

5.39 It is expected that compliance costs for small business taxpayers and administrative costs for the ATO will be similar to those presently being experience.

5.40 The Treasury and the ATO will monitor these taxation measures on an ongoing basis.

5.41 The amendment contained in Schedule 5 Part 1 Item 2 to the Bill will amend the ITAA 1997 by inserting a rewrite of the small business roll-over rules. A roll-over allows deferral of a capital gain or loss until a later CGT event happens.

5.42 The amendment will also insert in the ITAA 1997, measures that extend the roll-over to land and buildings held by a taxpayer where the land and buildings are used by another entity connected with the taxpayer.

• Part A provides an explanation of the rules about small business roll-over.

• Part B discusses changes to the ITAA 1936.

• Part C lists provisions that have not been rewritten.

5.43 Division 17 of Part IIIA of the ITAA 1936 deals with roll-overs for a CGT event happening to an asset of a small business where the taxpayer acquires new business assets. The general effect of the roll-over defers the determination of the capital gain until a CGT event happens to the new asset.

5.44 The roll-over is available if the net assets of the business entity, together with related entities, do not exceed $5 million in value.

5.45 Division 17A was inserted in the ITAA 1936 by the Taxation Laws Amendment Act (No. 1) 1997 (Act No. 122 of 1997). Amendments to this Division were made by Act No. 16 of 1998.

5.46 The measures will extend these provisions to assets held by a taxpayer that is not carrying on a business if the assets are used by another entity connected with the taxpayer in the course of carrying on a business. For example, a taxpayer owns land on which a plant nursery is carried on by the taxpayer’s family trust.

5.47 Division 17A is translated as Division 123. Two changes have been made to the substance of Division 17A in the course of its translation into the rewrite. The new Division 123 includes the extension to the small business roll-over and aligns the tax treatment of assets other than depreciable assets with that of depreciable assets. The later change removes the cost base adjustments that were required for the new business assets under Division 17A.

5.48 The JCPAA reviewed the rewritten ITAA 1936 provision contained in Act No. 46 of 1998. The JCPAA tabled their findings in Parliament on 12 March 1998 as Report 356: An Advisory Report on the Tax Law Improvement Bill (No. 2) 1997. Recommendation 3 of that report requested (among other things) delaying the introduction of the rewritten small business roll-over provisions pending further review by the JCPAA.

5.49 The JCPAA findings in that further review was tabled in Parliament on 21 December 1998 as Report 364: An Advisory Report on the Delayed Provisions of the Tax Law Improvement Bill (No. 2) 1997.

5.50 The amendments discussed in this Chapter reflect recommendation 3 of Report 356 and recommendations 4 and 5 of Report 364 made by the JCPAA.

5.51 The rewrite of the small business roll-over will apply to assessments for the 1998-99 income year and later income years. [Part 5, Item 35]. The date of effect accords with the view expressed by the JCPAA in Report 364 paragraphs 2.9 to 2.12. The extension to the roll-over will apply to a CGT event happening to land and buildings after 13 August 1998. [New section 123-80]

5.52 Division 123 allows an optional roll-over where:

• a CGT event happens to an active asset (see paragraph 5.68), shares in a company or units in a unit trust;

• the CGT event would have resulted in an entity making a capital gain;

• the entity would have had a net capital gain for the year; and

• the entity chooses one or more replacement assets.

[New section 123-10]

5.53 The roll-over consists of the following elements:

• the amount of the capital gain (the notional capital gain) is disregarded to the extent it does not exceed the acquisition cost of the new business asset;

• the notional capital gain is offset against any capital losses of the current income year and net capital losses of previous income years, that would have been applied in calculating a net capital gain in respect of the asset.

[New sections 123-15, 123-25, 123-30, 123-35 and 123-40]

5.54 If the new business assets only consist of goodwill, the notional capital gain is disregarded from a CGT event happening to goodwill to the extent of the acquisition costs of acquiring new goodwill. [New section 123-30]

5.55 If none of the new business assets are goodwill, the notional capital gain is disregarded to the extent of the acquisition costs of the new business assets. [New section 123-35]

5.56 Where the new business assets consist of both goodwill and other assets, the notional capital gain from a CGT event happening to goodwill is disregarded to the extent of the acquisition costs of acquiring new goodwill.

5.57 Any remaining notional capital gain (from a CGT event happening to both goodwill and other assets) is disregarded to the extent of the acquisition costs of acquiring new assets that are not goodwill. Notional capital gains from assets other than goodwill can not be disregarded with respect to the acquisition costs of acquiring goodwill. [New section 123-40]

5.58 If a CGT event happens to a share in a company, the amount of the capital gain that can be applied is limited to a pro rata share of unrealised net capital gains from active assets of the company.

5.59 A corresponding rule applies if the asset is a unit in a unit trust. [New section 123-20]

5.60 If the new business assets are shares in a company or units in a unit trust, the extent to which the notional capital gains can be disregarded is the proportion of the market value of the total active assets, of the company or trust, those shares or units represent at the time of acquiring the shares or units. [New section 123-45]

5.61 An entity is eligible for roll-over if the total net value of the entity’s assets, assets of connected entities, and assets of certain associates (the small business CGT affiliate) do not exceed $5 million. [New section 123-50]

5.62 A small business CGT affiliate of a taxpayer is:

• if they are an individual, their spouse or child under 18; or

• a person that acts in accordance with the taxpayer’s wishes or in concert with the taxpayer.

5.63 Partners in a partnership will not be a small business CGT affiliate of another person merely because they act in concert. [New section 123-55]

5.64 The taxpayer’s and their small business CGT affiliate’s interest in another entity are combined to establish if the taxpayer has at least 50% interest in another entity. This control test is used for the purpose of determining whether 2 entities are connected entities. [New section 123-60]

5.65 A control test exists to determine whether:

• a taxpayer exceeds the $5 million threshold; or

• land and buildings held by the taxpayer are used by their connected entity or is their small business CGT affiliate.

5.66 A taxpayer will have a connected entity if:

• the taxpayer controls another entity;

• the other entity controls the taxpayer; or

• a third entity controls both the taxpayer and the other entity.

The test generally requires a taxpayer to have at least 50% interest in another entity. [New section 123-60]

5.67 For an asset to be eligible for roll-over, it must be:

• an active asset at the time of the CGT event happening and to have been an active asset for at least half the time it was owned by the entity claiming the roll-over;

• a share in an Australian resident private company of which the entity is the controlling individual; or

• a unit in an Australian resident unit trust, other than a publicly traded unit trust, of which the entity is the controlling individual. [New section 123-65]

5.68 An active asset is:

• one used, or held ready for use, by the entity in carrying on a business;

• an intangible asset such as goodwill that is inherently connected with that business; or

• land or a building the taxpayer holds and is used by its connected entity, or its small business CGT affiliate, in carrying on a business;

but not a share, an interest in a trust, an interest in a connected entity, a financial instrument or, an asset used predominantly to derive rent, interest, an annuity, royalties or foreign exchange gains.

5.69 For land and buildings held by a taxpayer where the land and buildings are used by the taxpayer’s connected entity or small business CGT affiliate, a roll-over will only apply to CGT events happening after 13 August 1998. [New section 123-80]

5.70 An individual will be a controlling individual of a company if the individual:

• is a director or an employee of the company; and

• owns non-redeemable shares carrying at least 50% of the voting power and rights to distribution of income or capital.

5.71 To be a controlling individual of a unit trust the individual must be:

• an employee of the trust; and

• is beneficially entitled to at least 50% of the income and capital of the trust. [New section 123-70]

5.72 For a new business asset to qualify as a replacement asset it must be:

• an active asset, a share in a company or a unit in a unit trust; and

• acquired within the period commencing one year before and ending 2 years after the last CGT event happening within the income year for which roll-over is sought. [New subsections 123-75(1) and (2)]

5.73 If a replacement asset is a share in a company or a unit in a unit trust:

• the entity obtaining the roll-over must be the controlling individual of the company or unit trust and not be acting in the capacity of trustee; and

• the company or unit trust must be an Australian resident and at least 80% of its assets must be active assets. [New subsections 123-75(3) and (4)]

5.74 If the taxpayer obtaining the roll-over dies and a replacement asset passes:

• to the deceased’s personal legal representative – acts of the deceased in relation to the replacement asset are taken to be acts of the personal legal representative; or

• to the deceased’s beneficiary – acts of the deceased or the deceased’s personal legal representative in relation to the replacement asset are taken to be those of the beneficiary. [New section 123-85]

5.75 A CGT event happens if there is a change in the status of a CGT asset that was a replacement asset in a small business roll-over. For example, a replacement can change status by ceasing to be used as an active asset in the taxpayer’s business.

5.76 The taxpayer will make a capital gain equal to the amount of notional capital gain that was previously disregarded with respect to the replacement asset that changed status. The CGT event happens at the time of change. [Schedule 5 Part 3 Item 9, new section 104-185]

5.77 A CGT event happens where there is a change in the circumstances where a share in a company or a unit in a unit trust was a replacement asset in a small business roll-over. For example, a taxpayer ceases to be a controlling individual of the company in which the shares, as replacement asset, were acquired.

5.78 The taxpayer will make a capital gain equal to the amount of notional capital gain that was previously disregarded with respect to the acquisition costs of the shares or units. The CGT event happens at the time of change. [Schedule 5 Part 3 Item 9, new section 104-190]

5.79 The Treasurer announced in Press Release No. 76 of 1998 an extension to the small business roll-over relief. The extension allows the small business roll-over relief to apply to:

• land and buildings held by a taxpayer;

• used by its connected entity or small business CGT affiliate in the course of carrying on a business; and

• a CGT event happens to the land or buildings after 13 August 1998.

5.80 The extension to the small business roll-over was achieved by modifying the definition of active assets to include such land and buildings. [New section 123-80]

5.81 The change to the definition of active asset required a consequential change to the calculation of the $5 million net asset value threshold. The amendment ensures that a small business CGT affiliate’s assets are taken into account for the $5 million threshold if a taxpayer seeks a roll-over or retirement exemption for land and buildings it holds is used by their small business CGT affiliate in carrying on a business. [New sections 118-440 and 123-50]

5.82 The existing small business roll-over provisions provides for the cost base of a replacement asset (other than depreciable assets) to be reduced by the amount of capital gain arising from a CGT event happening to a small business asset. The cost base could not be reduced to a negative amount.

5.83 When CGT event J2 or J3 happens to the replacement asset the cost base of that asset is restored. That is, the prior reduction is reversed. The amount the cost base is restored by is taken to have been incurred at the time of CGT event J2 or J3 happening.

5.84 The cost base adjustment resulted in the following consequences:

• taxpayers incurred additional compliance costs; and

• taxpayers were denied indexation of the amount the cost base is restored by for the period from when the cost base was initially reduced to when it is restored.

5.85 The rewrite aligned the tax treatment of assets other than depreciable assets with that of depreciable asset. This was achieved by removing the cost base adjustment for assets other than depreciable assets. This change will benefit the taxpayer by:

• removing the additional compliance costs caused by the prior cost base adjustment; and

• giving full access to indexation of the cost base of a replacement asset.

[Schedule 5 Part 3 Item 9, new sections 104-185 and 104-190]

|

Provision

|

Subject

|

Reason for omission

|

|---|---|---|

|

160ZZPJA

|

Application provision continuing operation of Division 17A to assessment

for income years beyond 1997-98

|

Operation of Division 17A closed off due to inserting the rewritten

Division in the ITAA 1997.

|